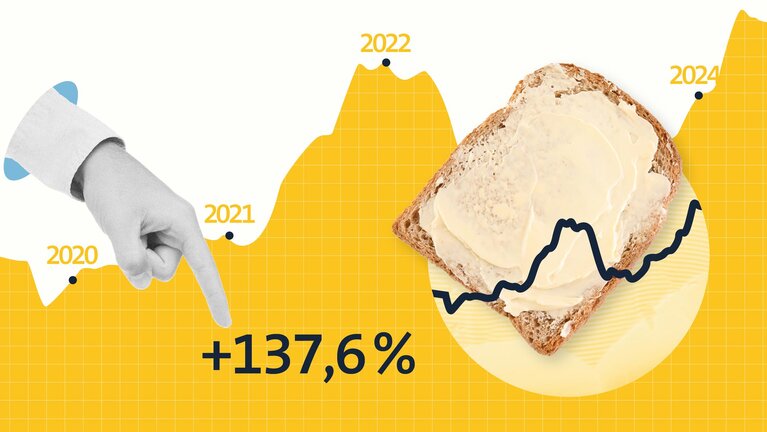

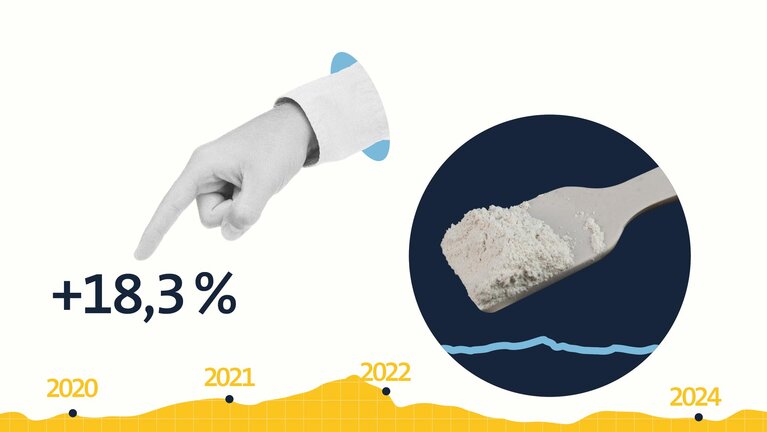

“After an initially stable development, the dairy market in 2024 became very volatile from autumn onwards. This was mainly due to increased cheese production, which required a lot of raw materials, so that stocks of butter and skimmed milk powder were already much lower in the first half of the year than in previous years, despite a slight initial increase in milk supply.

From mid-year onwards, the bluetongue outbreak reduced milk production to a greater extent and milk became scarcer. The result: A renewed rise in spot market prices for milk and milk products from autumn onwards, especially for fatty products. Milk was used more for cheese than for butter and powder and for longer-term contracts in the food retail sector.

Looking ahead to 2025 and the forecasts are subject to risks, but the dairy market could remain robust overall despite numerous uncertainties and pandemic influences. As the year draws to a close, producer stocks are likely to remain relatively low. At the same time, the decline in dairy cow numbers and the impact of bluetongue are likely to dampen milk production. This would initially limit the availability of raw materials, while cheese production would remain high, suggesting comparatively high prices. What happens next will depend on how milk production evolves and the extent to which price-driven demand responses affect sales of dairy products.”

„2025 will be another challenging year...”

“The rise in the cost of living is forcing consumers to be more price conscious. Despite falling inflation, living in Germany remains expensive. There are also industry-related challenges for the dairy sector; dairy products are losing popularity, especially among younger generations, who are increasingly turning to plant-based alternatives.

Nutrition trends are also evolving, with the ‘Nutrition Positivity’ trend focusing on a balanced, healthy diet. The 'Planetary Health' approach complements this trend with resource-efficient production.

Products designed to slow the ageing process are also gaining ground. Overall, there is a growing trend towards functional foods and dietary supplements that combine health claims with sustainability.

The situation for brand manufacturers remains tense. Private label products are clearly benefiting from consumers' price-orientation, while brand products, despite increased promotional activity, are only able to slow, not stop, the decline in sales. Nevertheless, strong brands with a clear unique selling point can hold their own even in times of crisis. MILRAM, for example, is growing faster than the cheese market and outperforming private labels, thereby extending its market leadership.

It is assumed that the majority of consumers will not automatically return to established brand products by 2025. Brand manufacturers will therefore have to create stronger incentives to win back customers. Although these products are still seen as more innovative, after years of limited investment, there is increasing pressure to provide new impetus.”

„Consumers are still very price-sensitive”